Latest News

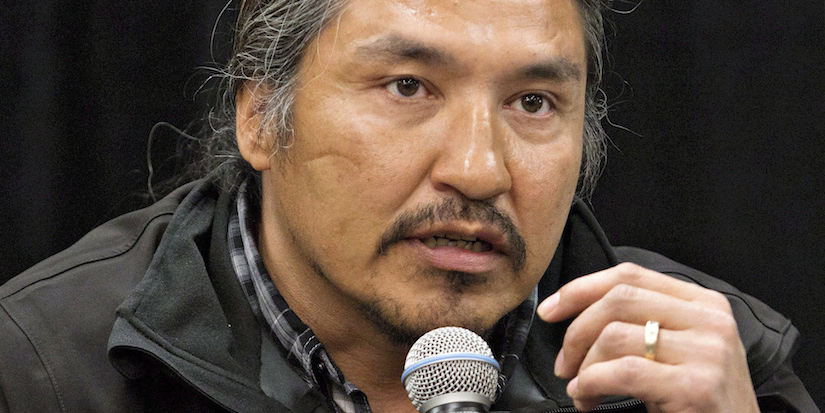

Ramon Solinas, regional marketing director.

Photo courtesy ‘Our City Tonight’

Insurance benefits made easy for small business

By Jim Gordon and Leeta Liepins

Published 2:34 PDT, Fri March 14, 2025

—

Our City Tonight sat down to talk about medical/dental insurance with Ramon Solinas, the Regional Marketing Director for Chambers of Commerce Group Insurance Plan for B.C. and Yukon. He has over 20 years of experience in the business.

OCT: We’ve had the privilege of talking to you before about a number of issues facing businesses and their employees. Tell us a bit more about the company before we get into the specific topic.

RS: The Chambers of Commerce Group Insurance Plan is a comprehensive employee benefit program that was specifically designed over 40 years ago to fill in the gap for coverage for the small to medium size businesses.

This program was created so that small to medium size businesses could access quality benefits and comprehensive benefits for their employees and their dependents. Today, we are over 30,000 members strong across Canada and are the number one association group insurance plan in the country.

OCT: One of the things that we really took away from speaking with you before in regard to insurance was that the perception was, that small businesses can’t afford an insurance benefit package for employees. But that really is not the case now.

RS: Not at all, and that’s the old school of thinking. The chambers plan specifically developed a program to service those needs. So, whether you are a one-person company or you have 50 or more employees, the chambers plan has products that are designed to service that specific market.

OCT: We want to dig a little deeper and talk about the specific services and how it is tailored to these businesses. You had mentioned something called the Health Spending Account or HSA. Please explain what this is and how this can literally be tailored to individual employees within the company.

RS: The HSA, is an individual account of money that an employer can set up for the employees with a pre-designated dollar amount. The employees can use that money for themselves and their dependents to spend on health and dental expenses that might happen unexpectedly.

The employee runs the expense through the health spending account. This can be for expenses that are not covered by the provincial government or perhaps that are not already covered by an existing or traditional employee benefit program.

OCT: What are some of the advantages for the employer and what are the advantages for the employees in this situation.

RS: If you take an older employee maybe they need some extra money for eyewear or vision care and maybe the younger employee has kids that they might need orthodontic treatment. If we try to package that all together in a traditional insurance benefit plan it becomes very, very expensive and very difficult.

With the health spending account, the advantage there is that you can customize. For example, the employees that need extra money for vision care they can easily spend their allotted funds for their eyeglasses.

Another example, an employee may run out of their $500 allotment for physiotherapy or chiropractic for the year and they need extra funds—they can use the health spending account to top that up.

For orthodontics, not all employees are going to have kids in that age group that need funds for that. The advantage for the employee is they can use the money for their specific needs and the advantage for the employer, they don’t have to try to cover off everything. They can just designate the money and again there’s the flexibility for the employees.

OCT: Why does a third-party need to be involved versus a firm just paying employees directly for their expenses?

RS: That’s a very good question, and one that we get asked a lot, when we’re in the field as to why the employee can’t just bring the receipts in and the business owner writes them a cheque for their medical expenses.

There are a few issues with that. The number one issue is, this would involve administration management for the business owner. And if it’s a small business, they must be out there doing what they do best—running their business and they would not have time for that extra burden of administration.

But more importantly, if it’s not run through a third-party through an insurance carrier, the reimbursement becomes a taxable benefit to the employee. If it’s run through the insurance company, a third party, then it becomes a non-taxable benefit to the employee.

OCT: Why is that the case?

RS: There is a small administration fee that is added on and so the way the CRA regulations go, once it flows through the insurance carrier with the administration fee, it gets viewed as an insurance premium.

If it is not being paid directly by the employer to the employee, and it’s run through a third-party, it gets treated as an insurance premium not as a direct pay for a benefit to the employee.

OCT: Can you explain if at year end there are funds carried over because they are not used that particular year, what happens to the funds.

RS: Another great thing about the health spending account for the employer is that there is flexibility. They retain the cost control on the pre-set amount that they have allotted for each employee.

For example, if they have allotted $2,000 a year for each employee to spend on medical and dental expenses. Some employees may not go through all that amount of money.

An employer report shows that the employee had not needed to use all that money and there’s some leftover, the employer then has a choice—to allow that employee to carry the leftover money into the new year or, the employer can set the program as a use it or lose it scenario.

So once again, there’s that flexibility for the employer to decide if they want to allow a carryover of the expenses.

For more information chamberplan.ca

2 Hours of free financial consulting

Jai Xin Planning Ltd.

C$120.00 C$0.00

Use any of our home staging service and get a second month rental for free!

MiiX Interiors

C$500.00 C$0.00

Get 10% off any order

Phantom Screens Lower Mainland

C$200.00 C$180.00